Investment comparison 2024: Best investments right now

The best investment right now depends on your investment horizon: For long-term investments, we consider rented real estate and broadly diversified equity ETFs to be the strongest combination of return and security.

Money that needs to be available in the short term belongs in an instant access savings account, fixed-term deposit, or a high-interest savings account – following the ECB’s key interest rate hike in June 2026, interest rates there are once again above 2 percent.

Gold is suitable as an addition to your portfolio, while Bitcoin is, at most, suitable in small doses for tech-savvy investors. Important before any investment: pay off consumer debt first, then build an emergency fund, then invest.

What is an investment – and what comes before it?

An investment is any use of money with the aim of preserving or increasing its value – from a savings account to ETFs to rented apartments. Which investment is the best cannot be answered in general terms, but only by looking at three questions:

- How long can you do without the money?

- How much fluctuation can you tolerate?

- And what return do you need to reach your goal?

Pay off debts first

Before thinking about investment options, you should pay off expensive debts. The interest rates on overdraft facilities and consumer loans are almost always significantly higher than the returns you can achieve with a safe investment. Every euro paid off is therefore the most profitable and, at the same time, risk-free investment of all.

Real estate loans and other loans that are part of an investment are excluded – here, borrowed capital works for you (more on this under leverage effect).

Then build an emergency fund

Keep three to six months’ worth of expenses as a reserve for broken washing machines, car repairs, or loss of income. This reserve must be available daily and therefore belongs in an instant access savings account – not in a brokerage account. Only what is left over beyond that should be invested in the medium and long term.

The magic triangle of investment

The magic triangle of investment is the most important mental model for investors. It describes three goals that any investment can only partially fulfill at the same time:

- Return: What does the investment yield – interest, dividends, rent, or capital appreciation?

- Security: How likely are losses up to a total loss?

- Liquidity: How quickly can you access your money again?

The triangle is called “magic” because it is impossible to maximize all three corners at once. A safe investment with high interest and daily availability does not exist – anyone promising you exactly that is concealing a risk or running a scam. Simply explained with examples:

| Example | Return | Security | Liquidity |

|---|---|---|---|

| Instant access deposit | Low | Very high | Very high (available daily) |

| 3-year fixed deposit | Medium | Very high | Low (tied to term) |

| Equity ETF | High | Medium (price fluctuations) | High (tradable every stock market day) |

| Rented real estate | High | High (real asset, land register) | Low (sale takes months) |

Some expand the model to the magic quadrangle of investment and add sustainability as a fourth objective. A detailed explanation with further examples can be found in our article on the magic triangle of investment.

Inflation: the silent opponent of every investment

States and central banks aim for an inflation rate of around 2 percent per year – as a safety margin against dreaded deflation, in which consumers postpone purchases and the economy stalls. For savers, this means: your money loses purchasing power according to plan.

In times of crisis, it happens faster: in 2022/2023, inflation temporarily reached almost 9 percent, and in 2026, inflation in the euro area is again noticeably above the target at around 3 percent. Current figures for Germany are published monthly by the Federal Statistical Office.

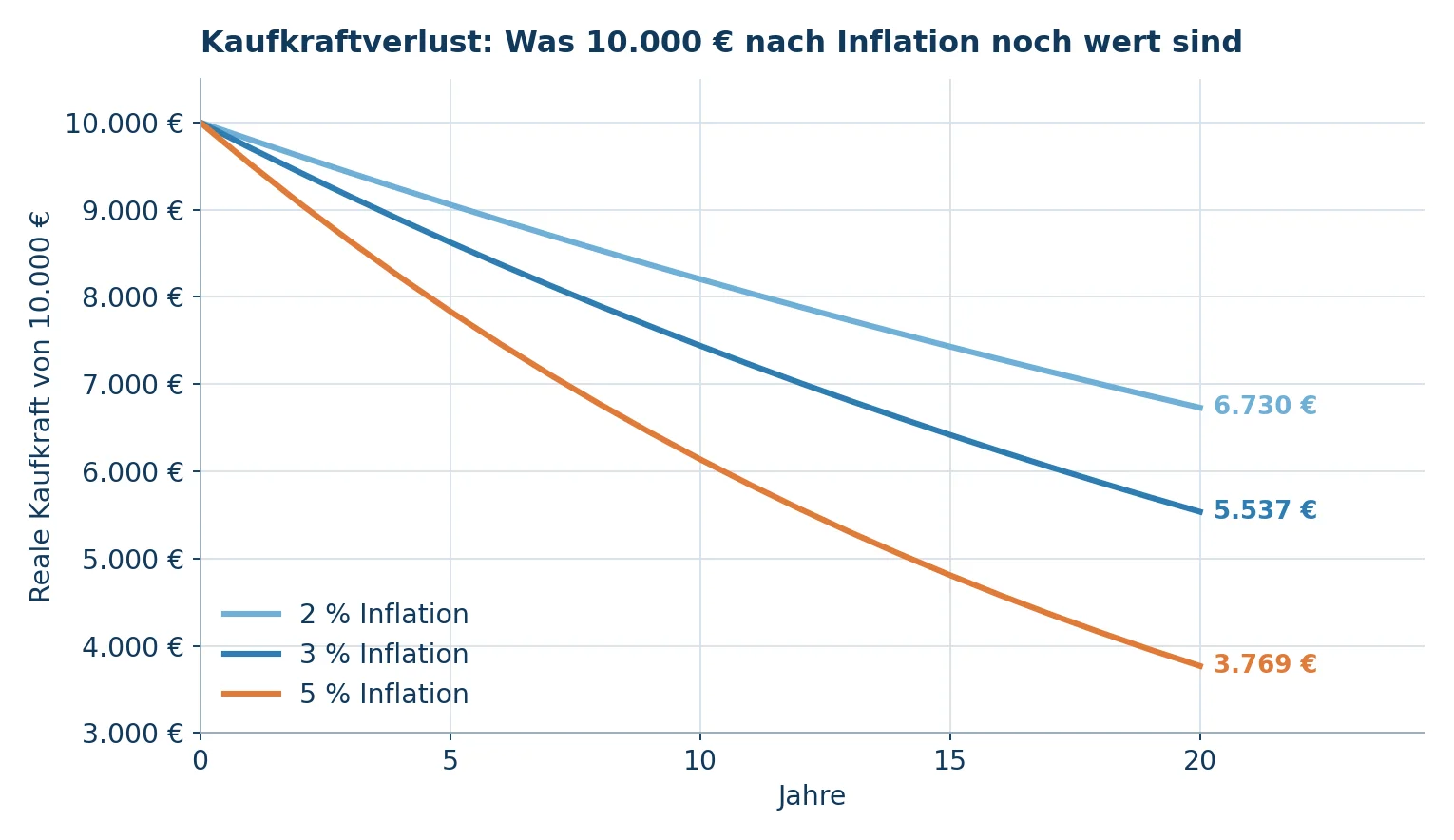

A simple sample calculation shows how strong currency devaluation is: €10,000 in a non-interest-bearing account has a purchasing power of only around €7,440 after 10 years at 3 percent inflation, and after 20 years only about €5,540 – almost a halving.

Real purchasing power of €10,000 over 20 years at 2 %, 3 %, and 5 % inflation (own calculation and representation)

This leads to the most important rule for any investment strategy: only when the return after costs and taxes is above the inflation rate does your wealth grow in real terms. There is no inflation-proof investment in the strict sense – but real assets such as real estate, stocks, and gold have historically preserved purchasing power much better than nominal values such as savings passbooks and cash.

Fixed-income investments are therefore not yield instruments, but ways to park money largely protected from inflation.

Current investment interest rates: What the ECB decision means for savers

On June 11, 2026, the European Central Bank raised key interest rates for the first time in three years: the deposit facility rate, which is decisive for savers, has been at 2.25 percent since June 17, 2026. The background is inflation in the euro area rising to over 3 percent.

For further interest rate trends in 2026, many observers expect one or two additional rate hikes, provided inflation does not ease – this is not guaranteed. The applicable key interest rates are officially published by the ECB.

Specifically for your investment, this means: interest rates for instant access deposits, fixed deposits, and savings accounts are rising again. The best instant access offers are currently at a good 2 to 2.5 percent, while fixed deposits currently yield around 2.5 to 3 percent depending on the term. However, banks pass on interest rate increases at different speeds – which is why comparing investment interest rates is particularly worthwhile right now.

What average interest rates banks in Germany actually pay is shown by the interest rate statistics of the Deutsche Bundesbank.

Short-term investments: Savings accounts, instant access deposits, and fixed deposits

A short-term investment makes sense whenever you need the money in the foreseeable future – for an emergency fund, a planned purchase, or as a transitional solution, such as between selling a house and buying a new one. Crucial factors here are security and availability, not maximum return.

The following applies to all three products: within the EU, deposits up to €100,000 per customer and bank are protected by law (details in the deposit protection section below).

Savings passbooks and savings accounts

The classic savings passbook is nowadays mostly a savings account without a physical book. It generally offers a three-month notice period for amounts over €2,000 and often yields slightly better interest than instant access deposits for existing customers of the same bank. Compared to instant access deposits it is less flexible, and compared to fixed deposits it pays worse interest – as a standalone investment, the savings account is therefore hardly attractive anymore and primarily a matter of habit.

Return: 1/5 · Security: 5/5

Instant access deposits (Tagesgeld)

Instant access deposit is the most flexible interest-bearing investment: no term, no notice period, the money is available daily. In return, the bank can change the interest rate at any time, and many banks entice people with temporary introductory rates for new customers that drop significantly after a few months. Instant access is the top choice for an emergency fund and for money you might need again in the short term – for instance within a year.

Return: 2/5 · Security: 5/5

Fixed deposits (Festgeld)

With a fixed deposit, you invest an amount for a fixed term – from 3 months, 6 months, and 1 year up to 5 or 10 years. The interest rate is fixed for the entire term; in return, you cannot access the money early or can only do so at a loss. Fixed deposits usually offer the highest interest rates among safe fixed-income investments and are suitable for money with a clear date of intended use.

Flexibility is created by an interest rate ladder (also called the terrace model): instead of fixing €30,000 for 3 years, you divide €10,000 each across terms of 1, 2, and 3 years. Every year, one tranche becomes available, which you can spend or reinvest at the then valid rate – meaning you are neither fully tied down nor giving up returns if interest rates rise.

Return: 3/5 · Security: 5/5

Where to find daily updated conditions

Specific interest rates of individual banks quickly become outdated. Two continuously updated and independent sources are sufficient for an overview: Stiftung Warentest maintains continuously verified interest rate comparisons for…

…and only considers banks from countries with stable deposit protection schemes. In addition, the aforementioned interest rate statistics of the Bundesbank show which interest rates are paid on market average – if your offer is significantly below that, you should switch.

When does which short-term investment make sense?

| Time Period | Suitable Investment | Typical Situation |

|---|---|---|

| Available daily | Instant access deposit | Emergency fund, transitional solution, “parking depot” for undecided money |

| 3 to 6 months | Short fixed deposit or instant access deposit | Planned purchase, tax back-payment |

| 1 year | 12-month fixed deposit | Equity for a real estate purchase in the following year |

| 2 to 5 years | Fixed deposit ladder, possibly high-rating bonds | Medium-term investment with a fixed goal (car, renovation) |

Conversely, there is no legitimate short-term investment with high returns: anyone promising significantly more than the best fixed deposit rates for a few months is demanding significant risk – or running a scam.

Long-term investments: Real estate, stocks, ETFs, funds, and bonds

From an investment horizon of about 10 years, the picture flips: price fluctuations lose their terror because you can ride out weak phases, and the compound interest effect unfolds its full power.

For long-term investment, higher-yielding asset classes are therefore suitable options.

Real estate as an investment

Rented real estate, as a tangible asset, combines security with high yield potential. Its decisive advantage over all securities: banks readily accept real estate as loan collateral. Through debt financing, you leverage your equity return (leverage effect) – an effect hardly accessible to retail investors in this form with stocks.

Added to this are ongoing rental income, tax optimization options, and long-term appreciation, secured by entry in the land register at a German district court.

To be honest, the drawbacks of real estate as an investment include: high capital requirements or good creditworthiness as an entry barrier, purchasing side costs, administrative effort, concentration risk with only one property, and low liquidity – a sale takes months, not seconds.

Whether real estate is a good investment for you therefore depends on income, equity, and investment horizon. Read more in the article Real estate as a capital investment – or directly in a non-binding consultation.

Return: 4/5 · Security: 4/5

Stocks

Stocks represent corporate ownership and are historically one of the highest-yielding asset classes – with corresponding fluctuations. Spring 2025 showed it: after tariff announcements by the US government, US stocks in particular slumped significantly, only to reach new record highs within a few months.

Those who can ride out such phases are historically rewarded; those forced to sell at the bottom realize losses. Dividend stocks resemble real estate here: appreciation plus ongoing payouts. Growth stocks rely solely on capital gains. Single stocks require time, knowledge, and diversification across many titles – otherwise, stocks as an investment are more like speculation.

Return: 4/5 · Security: 2/5

ETFs

An ETF (Exchange Traded Fund) automatically tracks an index like the MSCI World – without expensive fund management. ETF investing is thus the easiest and cheapest way to invest broadly in stocks, and is also perfectly suited as an “investment for lazy people”: a savings plan on a global equity ETF is enough to participate in global economic growth.

Historically, the average return of global stock indices over long periods was around 6 to 8 percent per year – without any guarantee for the future.

Why are ETFs still not a risk-free investment?

- ETFs are based on stock prices: if the market crashes, the ETF crashes too – temporary losses of 30 to 50 percent are possible during crises.

- The popular MSCI World is heavily concentrated on US companies and specifically on a few tech corporations; buying it means betting on the continued dominance of the US.

- Easy tradeability tempts people to sell at the worst possible moment.

ETFs beat real estate in terms of costs, entry barriers, and liquidity – real estate points ahead in stability, tax structuring, and debt leverage. Our recommendation is therefore not “either/or”, but both.

Return: 4/5 · Security: 3/5

Actively managed funds

Like ETFs, classic investment funds pool many securities – equity funds, bond funds, balanced funds, or real estate funds – but are actively managed. This usually costs 1.5 to 2 percent per year plus front-end loads.

Studies have shown for decades: after costs, only very few active funds permanently beat their benchmark index. As an investment, funds are therefore usually the more expensive version of an ETF – relevant primarily for niche strategies.

Return: 3/5 · Security: 3/5

Bonds

With bonds, you lend money to governments or corporations in exchange for fixed interest payments. Are bonds a good investment? As a fixed-income investment with predictable yields: yes – provided the debtor is sound.

German government bonds are considered extremely safe, but yield little; corporate bonds pay more, but carry default risk. In addition, bond prices fluctuate with interest rate levels: when interest rates rise, prices of existing bonds fall. For private investors, bonds are mainly interesting as a stability component in a portfolio.

Return: 3/5 · Security: 3/5

Gold, silver, crypto, and other alternative investments

Gold as an investment: Pros and cons

Gold has fascinated people for around 7,000 years and is considered by many to be the ultimate crisis-proof investment. The most important arguments at a glance:

- Pros: Gold is a globally recognized real asset without debtor default risk, often increases in price precisely when stocks fall, and has preserved purchasing power over centuries. In times of war and crisis, as well as inflation fears, demand – including from central banks – drives the price up.

- Cons: Gold pays neither interest nor dividends – return comes solely from the price, which can fluctuate wildly and is quoted in US dollars (currency risk). In addition, there are costs: a safety deposit box costs from around €100 per year, is often only available to account holders, and is frequently fully booked; storing at home happens at your own risk and should be coordinated with household insurance.

As an addition of 5 to 10 percent of total assets, gold can stabilize a portfolio – but as a standalone investment, it falls short. Anyone buying gold bars as an investment should choose common denominations (premiums drop significantly from 50 to 100 grams up) and deal only with certified dealers. Due to price fluctuations, we no longer rate security with the top score.

Return: 2/5 · Security: 4/5

Silver and other precious metals

Is silver a good investment? Silver is more of an industrial metal than gold (photovoltaics, electronics) and therefore fluctuates significantly more wildly. Furthermore, purchasing physical silver – unlike investment gold – incurs VAT, which burdens returns right from the start.

The same applies to platinum and palladium, whose prices depend heavily on the automotive industry. Precious metals as an investment beyond gold are therefore more speculative than a means of asset protection.

Return: 2/5 · Security: 3/5

Bitcoin and cryptocurrencies

Among cryptocurrencies, we consider at most Bitcoin to be debatable – as a highly speculative addition for tech-savvy investors, not as the foundation of an investment strategy. The risks remain substantial: extreme price volatility, potential state interventions in exchange to euros and dollars, an ecosystem that is confusing for laymen (keyword: tampered hardware wallets from third-party sellers), and third-party content permanently stored on the blockchain that could still become a problem.

Whether Bitcoin is a good investment ultimately depends on your risk tolerance: only invest money whose total loss you could stomach.

Return: 4/5 · Security: 1/5

Collectibles: Whisky, watches, diamonds, wine, and Lego

By collectibles, we mean tangible real assets you can touch: luxury watches like Rolex, whisky (up to whole whisky casks), wine, art, rare Lego sets, or diamonds. The appeal lies in personal affinity – the return is a matter of luck.

Markets are opaque, driven by trends, and illiquid: there is no exchange, and sales run through dealers and auctions with high markdowns. Are diamonds a good investment? For non-experts, no – without certificates and expert knowledge, a fair price can hardly be determined, and the resale value is routinely well below the purchase price. Buy such objects out of passion, not as retirement provision.

Return: 1/5 · Security: 2/5

Sustainable and green investments

If you want to combine returns with impact, you will find a growing range of options: ETFs based on ESG or SRI criteria, thematic funds for renewable energy, and direct participations in wind or photovoltaic projects. As a rule: sustainable ETFs work like classic ETFs with a filtered stock universe.

Caution, however, with closed-end funds in single wind or solar parks – these carry long capital lock-up periods and, in the worst case, total loss, as several bankruptcies of green issuers have demonstrated. What you should watch out for and how to spot greenwashing can be read in the article Investing sustainably.

Digital investment and investing with AI

Robo-advisors and increasingly AI-driven investment apps promise to manage your portfolio automatically. Behind them usually lies a rule-based ETF portfolio compiled according to a questionnaire on your risk tolerance and adjusted continuously – for fees typically ranging from 0.3 to 1 percent per year on top of ETF costs.

Even an AI-assisted investment cannot predict the future of the markets; it automates discipline, nothing more. Anyone confident in setting up a simple ETF savings plan themselves saves the fee. Those who would otherwise not start at all are better off with digital investing than doing nothing – a provider is only trustworthy with German or EU regulation and without return guarantees.

Investment comparison: all investment forms at a glance

The following table summarizes our rating of return and security (own assessment, 1 = poor, 5 = very good):

| Investment Form | Return | Security |

|---|---|---|

| Savings passbook / savings account | 1/5 | 5/5 |

| Instant access deposit | 2/5 | 5/5 |

| Fixed deposit | 3/5 | 5/5 |

| Rented real estate | 4/5 | 4/5 |

| Stocks (individual titles) | 4/5 | 2/5 |

| Bonds | 3/5 | 3/5 |

| Active funds | 3/5 | 3/5 |

| ETFs | 4/5 | 3/5 |

| Bitcoin | 4/5 | 1/5 |

| Gold | 2/5 | 4/5 |

| Silver / precious metals | 2/5 | 3/5 |

| Collectibles (watches, whisky, etc.) | 1/5 | 2/5 |

Which investment fits which investment horizon?

The investment horizon is the period during which your money can remain tied up. The longer it is, the more worthwhile higher-yielding, albeit more volatile, investments become:

| Investment Form | Short-term (up to approx. 3 years) | Medium-term (approx. 3–10 years) | Long-term (10 years and more) |

|---|---|---|---|

| Instant access deposit / savings account | ✔ | (✔) | – |

| Fixed deposit | ✔ | ✔ | – |

| Bonds | – | ✔ | ✔ |

| ETFs / stocks / funds | – | (✔) | ✔ |

| Rented real estate | – | (✔) | ✔ |

| Gold | – | ✔ | ✔ |

| Bitcoin / collectibles | – | – | (✔) only as addition |

As a rule of thumb for 10 years and more: the best investment for 10 years is a combination of real assets – ETFs and/or real estate – with a safety buffer of interest-bearing accounts. For 5 years, fixed deposits and bonds dominate; a pure stock investment is already risky over 5 years because a crisis at the end of the term can wipe out returns.

Sample calculations: What interest and returns mean long-term

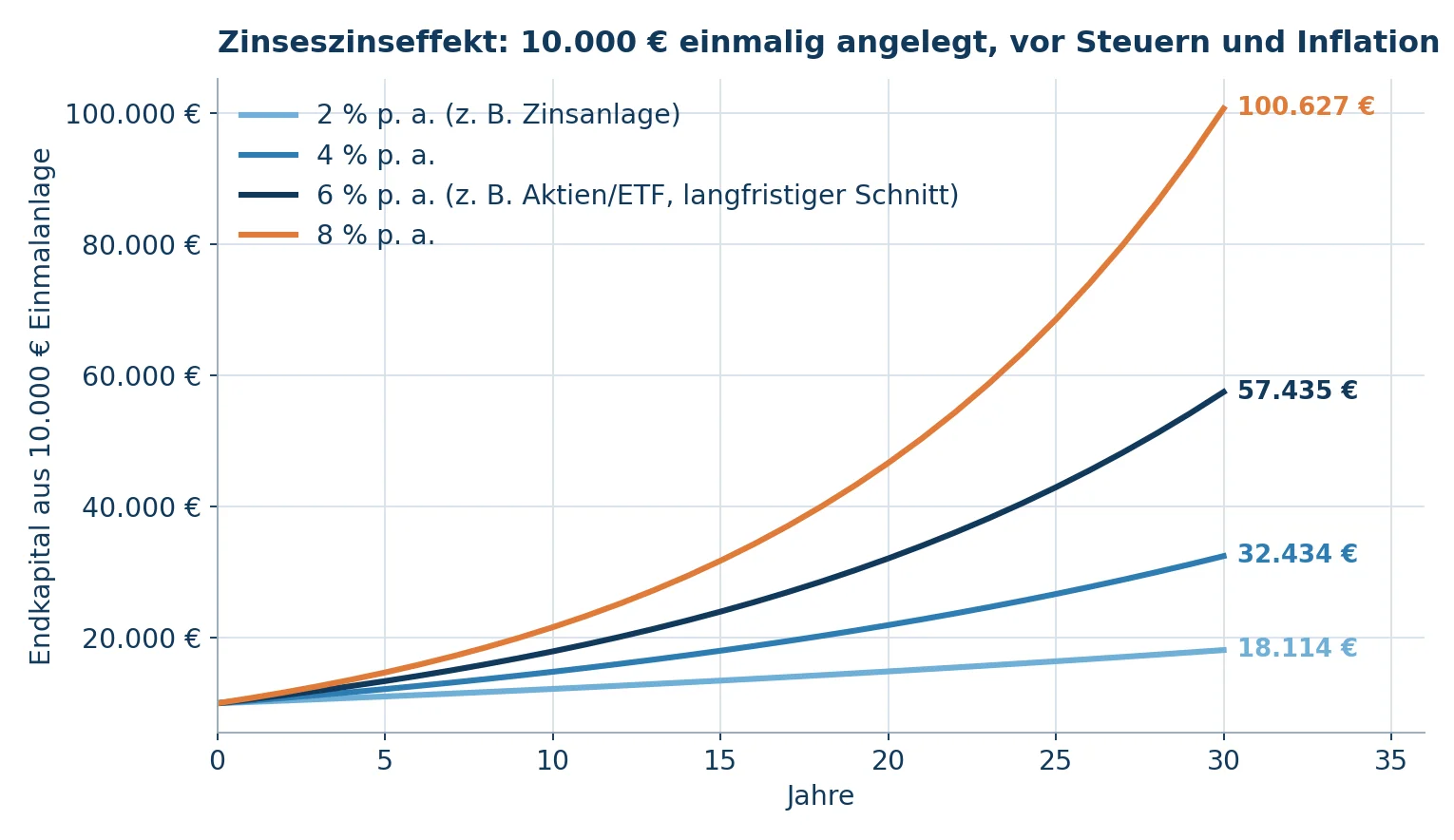

How large the difference between 2, 4, and 6 percent return really is, is underestimated by most – the compound interest effect works exponentially. The sample calculation for a lump-sum investment of €10,000 (before taxes and inflation):

| Return p. a. | After 10 years | After 20 years | After 30 years |

|---|---|---|---|

| 2 % (fixed-income investment) | €12,190 | €14,859 | €18,114 |

| 4 % | €14,802 | €21,911 | €32,434 |

| 6 % (stocks/ETF, long-term average) | €17,908 | €32,071 | €57,435 |

| 8 % | €21,589 | €46,610 | €100,627 |

Line chart: Value development of €10,000 over 30 years at 2, 4, 6, and 8 percent return

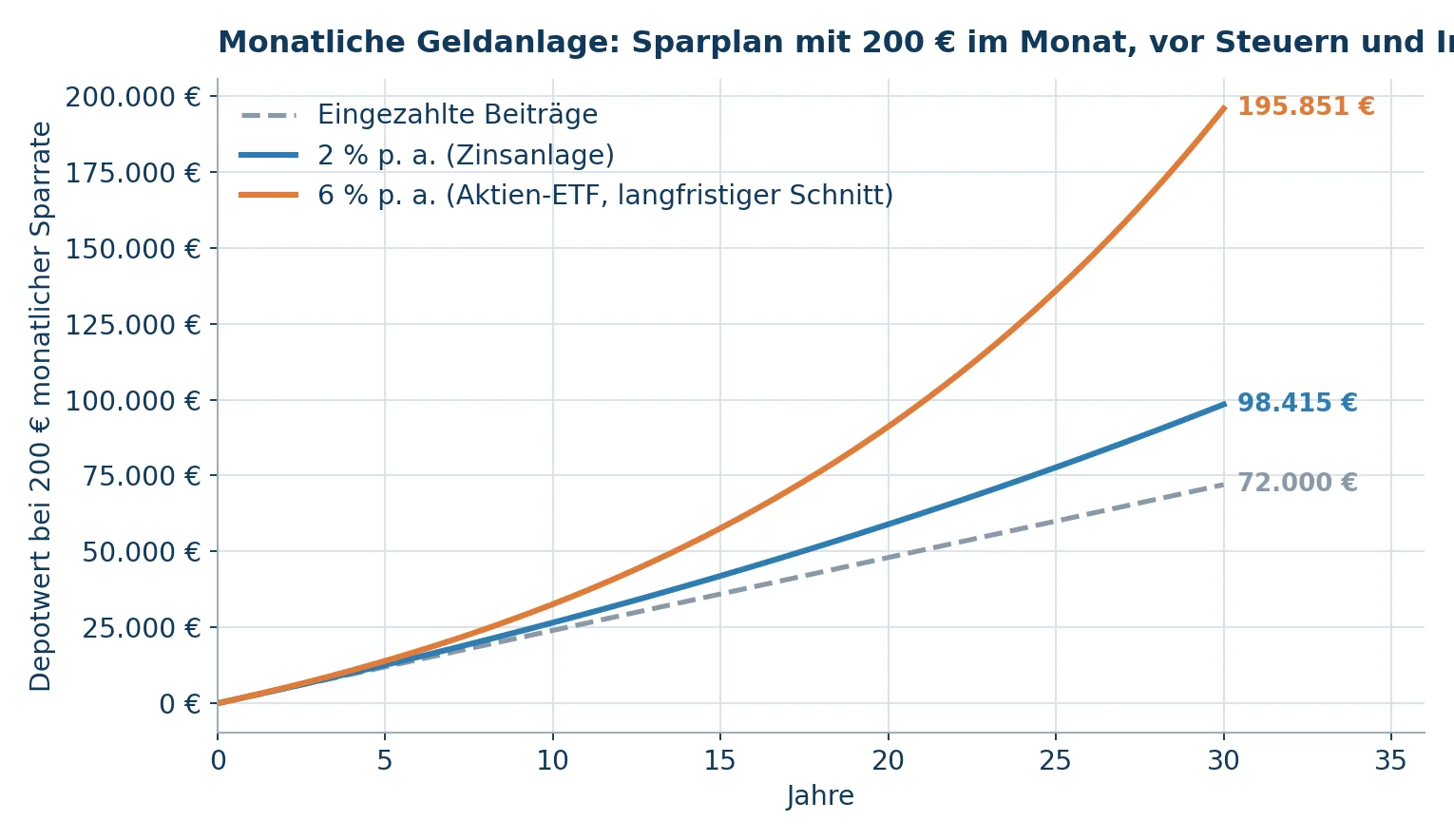

The effect becomes even clearer with monthly savings plans: setting aside €200 a month for 30 years means paying in a total of €72,000. At 2 percent interest, this grows to around €98,000 – at a 6 percent average ETF return, however, to about €196,000, i.e. double. Anyone wishing to calculate an investment can find neutral interest and savings calculators at organizations like the Consumer Advice Centers.

Savings plan with €200 monthly: contributions paid in compared to 2 % and 6 % return p. a. (own calculation and representation)

Investment with monthly payout

The reverse case is particularly interesting for retirees: an investment with a monthly payout. In a withdrawal plan, a capital stock is invested with interest and consumed in fixed installments. Sample calculation: €100,000 invested at 3 percent lasts about 23 years with a monthly withdrawal of €500. Without interest, the capital would be exhausted after just under 17 years.

Alternatives are distributing ETFs (fluctuating, but overall growing income), rental income from a property, or private annuity insurance with lifelong payments – though the latter buys its guarantee at the price of significantly lower returns and high costs, which is why annuity insurance rarely convinces as a pure investment.

Safe investments: Deposit protection, risk classes, and fraud protection

How safe is money in the bank?

Balances in savings passbooks, instant access deposits, and fixed deposit accounts are protected by law up to €100,000 per customer and bank across the EU – in Germany regulated in the Deposit Guarantee Act; details are explained by the financial supervisor BaFin.

If you want to safely invest more than €100,000 – for example, an investment of €200,000 after selling a house – simply distribute the money across multiple banks.

However, you should not rely blindly on European harmonization: in an emergency, the national guarantee scheme is liable first, and it is only as strong as the backing state. Stiftung Warentest therefore recommends limiting yourself to banks from economically strong Northern and Western European countries. A bonus is the additional voluntary deposit protection of German banks via the Deposit Protection Fund of the Association of German Banks.

Foreign setups such as investments in Switzerland, Liechtenstein, or Luxembourg offer retail investors hardly any advantages today: earnings are fully taxable in Germany, and Swiss Franc accounts merely add currency risk to your savings goal.

Risk classes of investments

Banks and brokers categorize investment products into risk classes – usually from 1 (safety-oriented: instant access, fixed deposit) to 5 (speculative: options, crypto). The classification helps with self-assessment: a conservative investment operates in classes 1 to 2, a balanced portfolio mixes classes 1 to 3, and anyone adding higher classes needs time and nerve. What matters is that the risk class of your overall wealth matches your investment horizon – not that of every single product.

Recognizing investment scams

Where interest rates make headlines again, fraud schemes flourish: fake fixed deposit comparison portals, alleged AI trading platforms advertised by celebrities, shock calls from fake bank staff. Warning signs are always the same – guaranteed high returns with no risk, time pressure, payment to foreign accounts or in crypto, lack of a German regulatory license.

Before transferring any money, check providers in the company database of BaFin, which also publishes ongoing warnings about specific providers. A reputable investment never requires time pressure.

Crisis-proof investments – even in the event of war?

Since the outbreak of war in the Middle East, many investors have been asking for the ultimate crisis-proof investment. The honest answer: absolute security does not exist; diversification is the best protection. Broadly diversified real assets – real estate, global stocks, a gold allocation – combined with liquid reserves have proven effective in times of crisis. Panic selling and concentrated bets on a single “crisis asset”, by contrast, have historically cost investors returns time and again.

The right investment for every stage of life

Investments for beginners and young people

For beginners, students, and young people: the time advantage is your greatest capital. Even €25 or €50 a month in a global ETF savings plan leverages compound interest over decades – meaning investing works even with little money.

The order of priority to start: pay off overdrafts, put emergency funds into instant access deposits, then set up an ETF savings plan and let it run. Beginners can safely skip hot stock tips, crypto hypes, and complicated certificates. Incidentally, due to longer life expectancy and more frequent career breaks, women should consider investing more rather than less in stocks – the products themselves are the same.

Investments for children and grandchildren

Children have the longest investment horizon of all – the best investment for children, despite all fluctuations, is therefore a broadly diversified global equity ETF via savings plan. Grandparents can also provide for grandchildren or godchildren this way. Two points need to be clarified:

- If the account runs in the child’s name, the money irrevocably belongs to the child, but their own tax allowances can be used (saver’s allowance plus basic tax-free allowance – combined, five-figure annual capital gains remain tax-free).

- If it runs in your name, you retain control, but pay taxes yourself. For larger sums, gifted or inherited real estate also displays its special tax status. All details can be found in the article Investing money for children.

Best investment for retirees and seniors

In retirement, the goal shifts from wealth accumulation to wealth preservation with predictable withdrawals – but beware of the reflex to go “only savings accounts in old age”: someone investing at age 70 statistically has 15 or more years ahead of them in which inflation will erode capital. A layered model makes sense:

| Component | Share (Guideline) | Suitable Products | Purpose |

|---|---|---|---|

| Liquidity reserve | approx. 10–20 % | Instant access deposit | Ongoing expenses, emergencies, daily available |

| Predictable withdrawals | approx. 30–50 % | Fixed deposit ladder, high-rating bonds | Safe payouts for the next 5–10 years |

| Return component | approx. 20–40 % | Global equity ETF, possibly rented real estate | Inflation protection for capital in later years |

| Optional | up to approx. 10 % | Gold | Crisis buffer |

The specific allocation depends on health, pension, inheritance plans, and risk appetite: at age 75 or 80, the security share moves further into focus; conversely, if the main intent is to pass on an inheritance, the stock share can remain high – the heirs’ investment horizon counts as well.

Particularly important for seniors: avoid non-cancelable products with long terms and high entry costs, which brokers often like to sell to older clients.

Investments at Sparkasse, Volksbank, Allianz & Co.

Many investors specifically seek the best investment at their primary bank – Sparkasse, Volksbank, or institutions like Commerzbank, ING, DKB, Targobank, or Postbank – or at insurers like Allianz, Debeka, and Ergo, which offer fixed-deposit-like products and treasury bonds with terms of 1 to 12 years. Generally, nothing speaks against these providers, but you should keep three things in mind:

- Branch banks often pay less on instant access and savings accounts than specialized direct banks – the price for maintaining a branch network. Whether your local Sparkasse’s interest rates are competitive is shown by comparing them with the continuously updated interest rate comparisons linked above.

- Bank advisors are salespeople: in-house funds and commission-bearing insurance products are preferred choices. Always ask for all costs per year – and compare with a simple ETF.

- Insurance investment products often link investments to long commitment periods. Interest rate guarantees may seem attractive; but do the math on what remains after costs, and check whether a simple fixed deposit with statutory deposit protection achieves the same thing more cheaply.

In short: what constitutes the best investment at Sparkasse is not decided by Sparkasse, but by comparison with the overall market.

Taxes: What remains of your investment return

Interest, dividends, and realized capital gains are subject to a flat-rate withholding tax (Abgeltungsteuer) of 25 percent plus solidarity surcharge and, if applicable, church tax (§ 20 EStG).

Capital gains remain tax-free up to the saver’s allowance of €1,000 per person per year (€2,000 for joint assessment) – provided an exemption order (Freistellungsauftrag) has been submitted to the bank.

A completely tax-free investment for larger assets does not exist, but tax-optimized investing is very well possible: use tax allowances for all family members, employ accumulating ETFs for tax deferral – and with real estate, strategically plan depreciation as well as tax-free sales after a 10-year holding period (Saving taxes with real estate).

Best investment in 2026: our recommendation by investor type

What investors in Germany prefer for wealth building is surveyed annually by the Savings Banks Association in its Wealth Barometer: stocks, funds, and rented real estate have ranked high near the top for years – while the traditional savings passbook continuously loses approval. This aligns with our assessment. Here is how to find your personal best investment in 2026:

| Your Situation | Recommendation |

|---|---|

| Money is needed within 1–3 years | Instant access and fixed deposit – currently back above 2 % interest |

| Wealth building over 10+ years, small budget | Savings plan on a global equity ETF, starting at €25 monthly |

| Good income and/or equity available | Rented real estate with debt leverage, supplemented by ETFs |

| Retirement, focus on withdrawals | Layered model of instant access, fixed deposit ladder, and ETF portion |

| Safety-oriented, no risk of loss desired | Fixed deposit with banks boasting strong deposit protection – with conscious waiver of real returns |

Real estate and ETFs are not competitors, but partners: ETFs provide flexibility and low entry barriers, while real estate provides leverage, stable rental income, tax advantages, and the security of the land register – while creating living space on the side.

Whether an investment property fits your situation is something we are happy to clarify in a non-binding consultation. This is not about real estate funds, REITs, or other financial products, but about your own apartment with land register entry, notary, and everything that goes with it.